Neil Cooper-Smith, senior analyst, Business Pilot

The Business Pilot Barometer offers monthly analysis of the key trends defining window and door retail. It draws on real industry data collated by Business Pilot, the cloud-based business management tool developed by installers, for installers.

To put things into context, at the end of January, the Bank of England’s rep said that it now believes the downturn will be shorter and shallower than it initially feared. Inflation remains a problem, which is why, despite this modestly sunnier outlook, interest rates have increased to 4%.

In the same week, the International Monetary Fund put its own number on UK economic contraction: 0.6%. It attributed this to high energy prices, increased taxes, the high cost of labour and rising mortgage prices. These conditions have contributed, according to the GFK Index, to a three-point fall in consumer confidence in January to -45, a near historically low level.

At the same time, housebuilders were writing to the chancellor, calling for a return of the Help to Buy Scheme. This, they argue, would “light a fire under a slowing housing market” and avert a dramatic plunge in the supply of new homes.

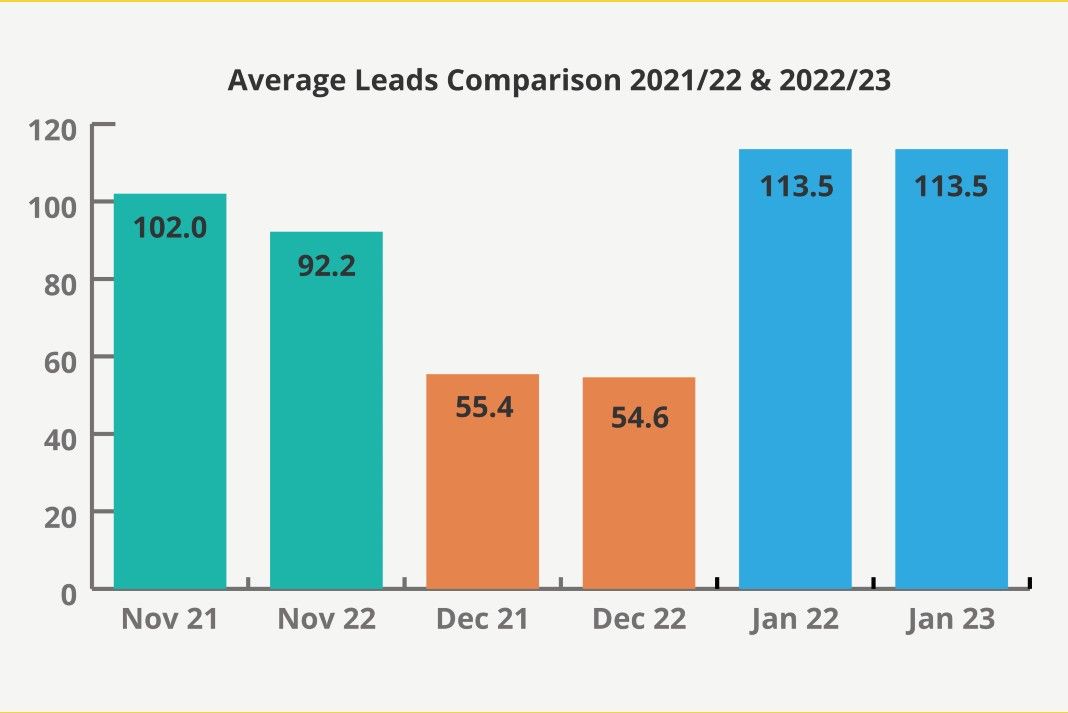

Despite this, window and door sales rebounded from the 43% seasonal fall seen in December with a 67% jump. Average leads more than doubled, up 108% from 55 to 114. The only negative was a 30% fall in average order values to £4,415.

What is the year-on-year change? Well, there isn’t! Average leads in January 2023 were identical to those in January 2022, at 113.5. Sales were almost identical at 40 and 41. Even average order values mirrored each other at £4,415 and £4,417. This is despite the economic context and far stronger economic head winds this time around.

What is the year-on-year change? Well, there isn’t! Average leads in January 2023 were identical to those in January 2022, at 113.5. Sales were almost identical at 40 and 41. Even average order values mirrored each other at £4,415 and £4,417. This is despite the economic context and far stronger economic head winds this time around.

It’s worth noting that although the energy crisis was looming on the horizon, in January 2022 the energy price cap hadn’t been raised, the energy price guarantee didn’t exist, Russia hadn’t invaded Ukraine and UK inflation was still at, in comparison to today’s figure, a respectable 5.5%.

So, can we draw down on this and predict with any confidence that 2023 is in fact not going to be so bad after all? Are we in for a repeat of 2022 – a year which, on balance, was… well, OK?

I’m not convinced we can make that prediction because the market context is so very different. But what we can say is that the market remains resilient, and it has confounded expectations and economic context repeatedly since 2019.

Sales drivers this time around are more pronounced. Distress purchases remain important but energy efficiency has assumed greater importance. The more casual discretionary spend that was still with us at the start of 2022 is less likely to be there in the face of pressure on household finances.

The flip side is that high energy costs give homeowners who were biding their time and waiting for the Covid-19-driven boom in home improvement to ease, a reason to commit to spending. We’re helping Business Pilot customers to retarget those prospects that didn’t quite get across the line last year.

With Business Pilot, a lead is never lost. It’s there for next time. For more information, visit businesspilot.co.uk. industry industry